Back to News & Insights

Research | 03.8.2023

The EM Credit Opportunity

Market Is Constructive

- Global Trends: Since the start of the year, markets have priced in further rate hikes by the Fed on the back of stronger economic and stickier inflation data. This has led to a recent increase in volatility as measured by the MOVE index, which tracks the volatility of US rates markets. We believe the uptick in volatility presents an opportunity. We expect the Fed will again revise up its rate path projections at the March FOMC meeting, bringing the Fed and market into greater alignment. Greater alignment, post repricing, may reduce uncertainty and spur risk taking.

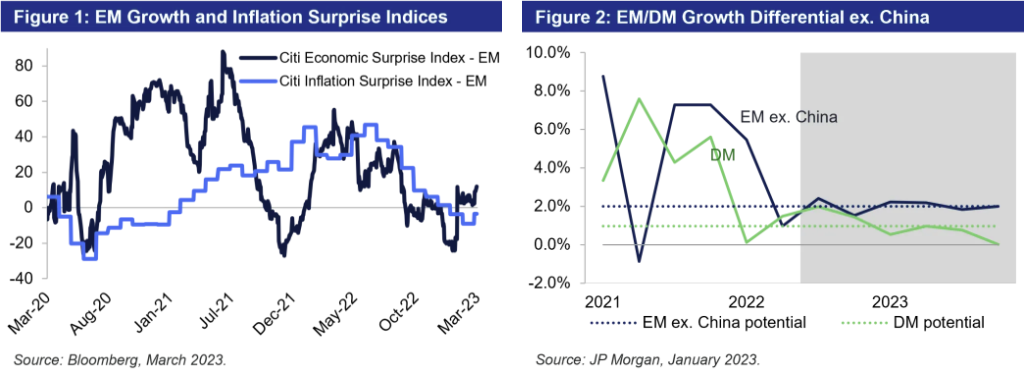

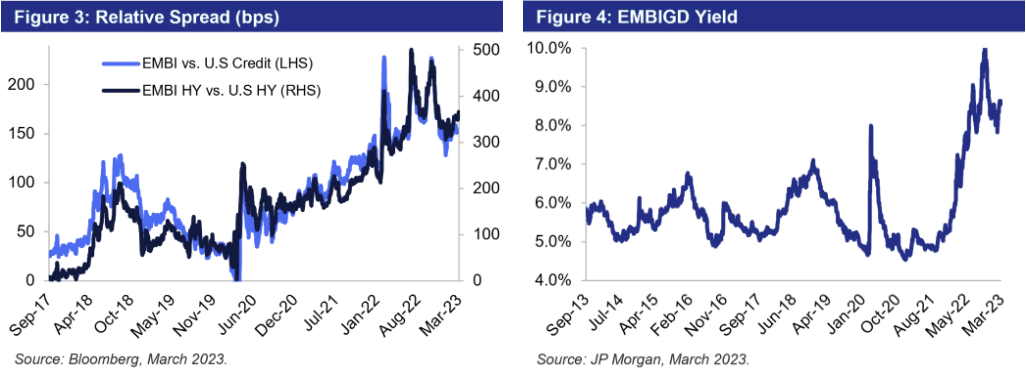

- EM Fundamentals: EM monetary policy tightening over the past two years support EM disinflation trends, while China’s re-opening and a consumption-led recovery have positive spillover effects for EM growth (Figure 1). All else equal, flows tend to follow high growth segments of the global economy. As per the latest JP Morgan forecasts for 2023, EM ex. China GDP growth is expected to outpace that of developed markets by approximately 2% and developed market growth is expected to be essentially flat (Figure 2). We have recently seen a number of growth estimate revisions pointing to higher China and Asia growth which should feed through to regional peers and broader EM.

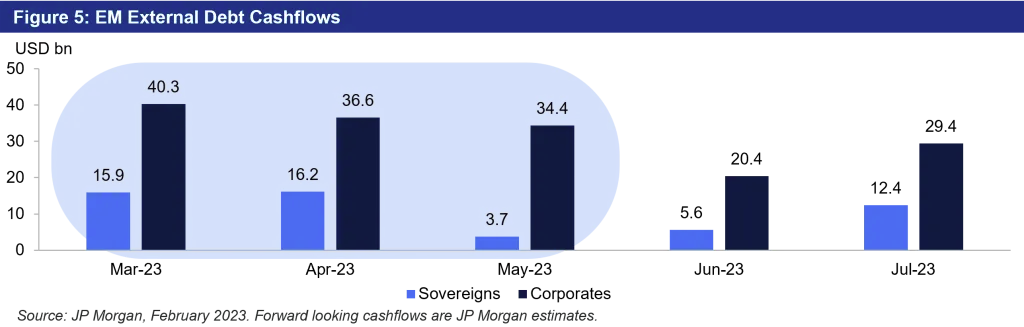

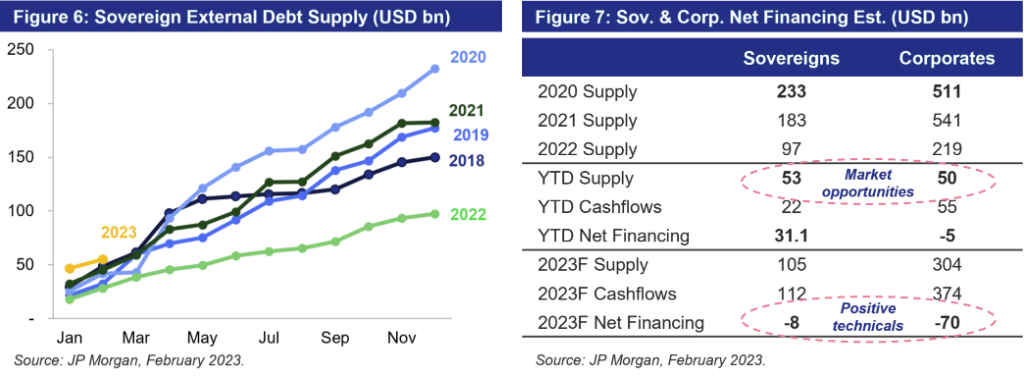

- Relative Value: EM fixed income continues to trade at attractive valuations to comparable public credit markets. EMBI (half-IG, half-HY) continues to trade at a 150 bps (“basis points”) spread pick-up to a comparable basket of U.S corporate credit. The EM high-yield segment in particular appears relatively cheap, with spreads for this segment trading 350 bps over U.S high yield (Figure 3). The yield of our asset class continues to hover close to its highest point in 10 years (Figure 4).

Technicals are Supportive

- Flows: Projected cashflows from outstanding EM external debt will be uniquely elevated for the next several months. The reinvestment of these proceeds provides natural demand for the asset class (Figure 5). More importantly, managers will seek to reinvest these proceeds in on-the-run liquid benchmarks and newly issued maturities that benefit from a high degree of liquidity and current yield. We expect projected cashflows to serve as a tailwind.

- Supply: The first month of the year marked a reanimation of the new issue market, offering investors opportunities to effectively rebalance and to capture concessionary pricing. Per JP Morgan estimates, sovereign supply in 2023 is expected to reach $105 billion, providing an expanded investment universe. At the same time, sovereign net financing- or the projected supply minus the cashflows from existing debt- is projected to be negative for a second consecutive year. Thus, while we expect to see more opportunities in primary markets, we still see this dearth of net-supply as highly constructive for outstanding valuations (Figure 7).

Certainly, risks remain with regards to the direction of rates driven by Fed policy action resulting from inflation metrics, the uneven nature of the global economic recovery post-Covid and the conflict in Ukraine, among others. Furthermore, timing the market will always be an imperfect exercise. That said, for a strategic allocation, we believe conditions remain highly constructive based on fundamentals, valuations, technicals and flows.

Disclaimers

This presentation and the information contained herein is provided by Marathon Asset Management, L.P. and its affiliates (together, “Marathon”) for educational and informational purposes only and does not constitute and should not be construed as an offering of advisory services or as an invitation, inducement, or offer to sell or solicitation of an offer to buy any securities, related financial instruments, or financial products in any jurisdiction.

This presentation is not research and should not be treated as research. This presentation does not represent valuation judgments with respect to any financial instrument, issuer, security, or sector that may be described or referenced herein and does not represent a formal or official view of Marathon.

The views expressed reflect the current views as of the date hereof, and Marathon does not undertake to advise you of any changes in the views expressed herein. It should not be assumed that Marathon will make investment recommendations in the future that are consistent with the views expressed herein or use any or all the methods of analysis described herein in managing client accounts. Marathon may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this presentation.

The contents hereof should not be construed as investment, legal, tax or other advice and you should consult your own advisers as to legal, business, tax and other matters related to the investments and business described herein.

The information in these materials does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein and may not be used or relied upon in evaluating the merits of investing therein. No such offer or solicitation will be made prior to the delivery of any applicable offering and related subscription or investment advisory materials (together, the “Offering or Advisory Materials”). Offers and sales will be made only pursuant to the Offering or Advisory Materials and in accordance with applicable securities laws.

The information contained herein has been compiled on a preliminary basis as of the dates indicated, and there is no obligation to update the information. The delivery of these materials will under no circumstances create any implication that the information herein has been updated or corrected as of any time subsequent to the date of publication or, as the case may be, the date as of which such information is stated. No representation or warranty, express or implied, is made as to the accuracy or completeness of the information contained herein, and nothing shall be relied upon as a promise or representation as to the future performance of the investments or business described herein.

This document is not intended to represent the rendering of accounting, tax, legal or regulatory advice. A change in the facts or circumstances of any transaction could materially affect the accounting, tax, legal or regulatory treatment for that transaction. The ultimate responsibility for the decision on the appropriate application of accounting, tax, legal and regulatory treatment rests with the investor and his, her or its accountants, tax and regulatory advisors. Investors should consult and must rely on their own professional tax, legal and regulatory advisors as to matters concerning the depicted fund, account or strategy and their investments in the fund, account or strategy. Prospective investors should inform themselves as to: (1) the legal requirements within their own jurisdictions for the purchase, holding or disposal of securities or other assets; (2) applicable foreign exchange restrictions; and (3) any income and other taxes which may apply to their purchase, holding and disposal of securities or other assets or payments in respect of the securities of any depicted fund, account or strategy.

By acceptance hereof, you agree that (i) the information contained herein may not be used, reproduced or distributed to others, in whole or in part, for any other purpose except as expressly provided herein without the prior written consent of Marathon; (ii) you will keep confidential all information contained herein not already in the public domain; and (iii) you will not use such information for any other purpose, including trading in the securities of Marathon-managed entities.

Some of the information used in preparing these materials may have been obtained from or through public or third-party sources. Marathon assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates or forecasts obtained from public or third-party sources, we have assumed that such estimates and forecasts have been reasonably prepared. In addition, certain information used in preparing these materials may include cached or stored information generated and stored by Marathon’s systems at a prior date. In some cases, such information may differ from information that would result were the data re-generated on a subsequent date for the same as-of date. Included analyses may, consequently, differ from those that would be presented if no cached information was used or relied upon.

AN INVESTMENT IN VEHICLES AND INSTRUMENTS OF THE KIND DESCRIBED HEREIN IS SPECULATIVE AND INVOLVES SUBSTANTIAL RISKS, INCLUDING, WITHOUT LIMITATION, RISK OF LOSS. YOU SHOULD CAREFULLY REVIEW THE DISCUSSION OF RISK FACTORS IN THE RELEVANT OFFERING DOCUMENT, SUBSCRIPTION MATERIALS, OR MANAGEMENT AGREEMENT BEFORE DECIDING TO INVEST.

Forward-Looking Statements: Some of the statements in this document constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. The forward looking statements in this presentation involve risks and uncertainties, including statements as to: (i) general volatility of the markets in which we invest; (ii) changes in our business strategy; (iii) availability, terms, and deployment of capital; (iv) availability of qualified personnel; (v) changes in our industry, interest rates, the securities markets or the general economy; (vi) increased rates of default and/or decreased recovery rates on our investments; (vii) changes in governmental regulations, tax rates, and similar matters; (viii) changes in generally accepted accounting principles by standard-setting bodies; and (ix) availability of investment opportunities. The forward-looking statements are based on our beliefs, assumptions, and expectations of our future performance, taking into account all information currently available to us. These beliefs, assumptions, and expectations can change as a result of many possible events or factors, not all of which are known to us or are within our control. If a change occurs, the performance of our portfolio and our business, financial condition, liquidity and results of operations may vary materially from those expressed, anticipated or contemplated in our forward-looking statements.

Definitions of Indices Referenced:

The J.P. Morgan Emerging Markets Global Diversified Index (EMBI Global Diversified) is a uniquely weighted version of the EMBI Global. It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by the EMBI Global.

The ICE BofA MOVE Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options. It is the weighted average of volatilities on the CT2, CT5, CT10, and CT30.